UK government bond yields drop as Sunak takes office

Investors have bought UK government debt, pushing down bond yields to the level seen before Liz Truss and Kwasi Kwarteng announced their disastrous “mini-budget”.

Prices on UK government debt, known as gilts, plummeted after Truss and Kwarteng announced steep tax cuts for the wealthy without saying how it would affect the government borrowing. Yields rise when prices fall.

The 30-year yield dropped as low as 3.64% on Tuesday, the level on September 22.

During the market chaos that followed the budget on 23 September, the 30-year gilt yield jumped above 4% as investors dumped UK government debt. Then there was a truly historic yield surge above 5% the next week that threatened to cause a spiralling crisis in UK pension funds.

The Bank of England was forced to intervene to prevent that happening, but it also prompted Conservative party MPs to dispense with Kwarteng as chancellor and then Truss as prime minister in a bid to restore calm. MPs also managed to see off a return by Boris Johnson.

Dean Turner, chief eurozone and UK economist at UBS Global Wealth Management, said:

The market reaction to Johnson’s withdrawal and Sunak’s win has seen gilt yields fall sharply across the curve, while the pound has been steady against the major crosses. Sunak’s victory will not call a halt to the political volatility in the UK, but the temperature should cool significantly.

Key events

Filters BETA

It’s a mixed picture on Wall Street today, with the tech-focused Nasdaq outperforming the broader market.

Here are the opening snaps from Reuters:

-

NASDAQ UP 54.32 POINTS, OR 0.50%, AT 11,006.93 AFTER MARKET OPEN

-

S&P 500 UP 6.32 POINTS, OR 0.17%, AT 3,803.66 AFTER MARKET OPEN

-

DOW JONES DOWN 43.91 POINTS, OR 0.14%, AT 31,455.71 AFTER MARKET OPEN

Coca-Cola enjoyed higher-than-expected sales in the third quarter as it raised prices around the world and predicted higher revenues for the year.

The US drinks company said it had pushed up revenues by raising prices and pushing buyers to more expensive drinks – defying concerns that consumers will cut back as the global economy slows.

Net revenues grew 10% to $11.1bn (£9.8bn), and it enjoyed 16% organic sales growth as well.

Its sugary drinks rival PepsiCo also raised forecasts for the year this month even as its costs rose. Sugary drinks have been among the last products to be cut back by price-conscious customers.

UK government bond yields drop as Sunak takes office

Investors have bought UK government debt, pushing down bond yields to the level seen before Liz Truss and Kwasi Kwarteng announced their disastrous “mini-budget”.

Prices on UK government debt, known as gilts, plummeted after Truss and Kwarteng announced steep tax cuts for the wealthy without saying how it would affect the government borrowing. Yields rise when prices fall.

The 30-year yield dropped as low as 3.64% on Tuesday, the level on September 22.

During the market chaos that followed the budget on 23 September, the 30-year gilt yield jumped above 4% as investors dumped UK government debt. Then there was a truly historic yield surge above 5% the next week that threatened to cause a spiralling crisis in UK pension funds.

The Bank of England was forced to intervene to prevent that happening, but it also prompted Conservative party MPs to dispense with Kwarteng as chancellor and then Truss as prime minister in a bid to restore calm. MPs also managed to see off a return by Boris Johnson.

Dean Turner, chief eurozone and UK economist at UBS Global Wealth Management, said:

The market reaction to Johnson’s withdrawal and Sunak’s win has seen gilt yields fall sharply across the curve, while the pound has been steady against the major crosses. Sunak’s victory will not call a halt to the political volatility in the UK, but the temperature should cool significantly.

Ryanair boss Michael O’Leary is never one to be shy with an opinion, and he has views on Rishi Sunak’s ascent to the premiership – or perhaps more accurately on Sunak’s predecessors.

O’Leary told Reuters on the sidelines of an event in Lisbon that he was glad “adults have taken charge again”. He said he hoped Sunak’s first decision would be to rejoin the EU free trade agreement, and said:

They are getting rid of some of the people who were there, from Boris Johnson to Liz Truss, all the Brexiteer wing of the Tory party – they are crazies.

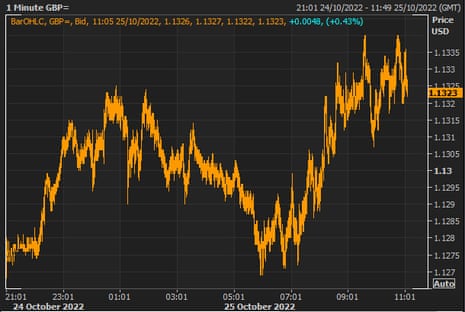

Sterling has gained more ground against the US dollar today: it is now up by 0.45% above $1.13.

The currency did not move much during Sunak’s speech: the messages about cutting the deficit through “difficult decisions” – likely a reference to spending cuts – have already been firmly communicated by chancellor Jeremy Hunt.

Another thing that could help reassure financial markets further would be an improvement in the UK government’s relationship with the EU.

Congratulations to @RishiSunak on your appointment as U.K. Prime Minister.

In these testing times for our continent, we count on a strong relationship with the U.K. to defend our common values, in full respect of our agreements.

— Ursula von der Leyen (@vonderleyen) October 25, 2022

Rishi Sunak has said the UK government faces “difficult decisions” ahead in his first address as prime minister.

Standing outside 10 Downing Street after meeting the King, Sunak said he would not leave the next generation with debt. As chancellor, Sunak oversaw all-time record deficits in response to the coronavirus pandemic and support the economy through lockdowns. He said:

The government I lead will not leave the next generation, your children and grandchildren, with a debt to settle that we were too weak to pay ourselves.

Chancellor Jeremy Hunt, who is expected although not confirmed to remain in post under Sunak, has already indicated that deep cuts to government spending are likely in a bid to calm the market turmoil caused by Liz Truss and Kwasi Kwarteng’s tax cuts that promised to broaden the UK’s government deficit.

You can follow more details from the speech and the reaction on the politics live blog here:

Adidas ends Kanye West partnership after antisemitic comments

Sarah Butler

Adidas has ended its partnership with Kanye West in the light of the rapper’s recent comments saying it “does not tolerate antisemitism.”

The German sports brand said the comments and actions from West, who is also known as Ye, had been “ unacceptable, hateful and dangerous, and they violate the company’s values of diversity and inclusion, mutual respect and fairness.”

The company said it would take a “short-term” hit of €250m (£219m) hit to its income for this year after taking the decision to end production fo Yeezy branded products and stop all payments to West and his companies stopping the brand’s business with immediate effect.

In 2020, the partnership brought in nearly $1.7bn in revenue, according to Bloomberg, and was set to expire in 2026.

The brand said it was the sole owner of all design rights to existing products as well as previous and new colorways under the Yeezy partnership.

Adidas’s move comes after Balenciaga, Gap and JPMorgan Chase all cut ties with West after repeated anti-Semitic remarks.

The rapper recently claimed that Adidas could not drop him despite his comments insighting calls for a boycott.

Manufacturers’ confidence drops the most since pandemic lockdowns – CBI

British manufacturers’ confidence dropped at the fastest pace since the first coronavirus lockdown, according to a poll of big companies by the Confederation of British Industry (CBI).

A balance of 48% of big manufacturers were pessimstic about the economy, compared to only 21% in the last survey in July. The last time optimism fell so low, aside from the depths of pandemic lockdowns, was during the global financial crisis of 2008-09, according to data published on Tuesday that suggested businesses are preparing for a tough time ahead.

The survey took place after Liz Truss and Kwasi Kwarteng unveiled their “mini-budget” that provoked financial market turmoil and their own removal from 10 Downing Street with unprecedented speed. And there is still the prospect of a long recession looming.

The CBI’s industrial trends data showed that output from UK manufacturers fell in the three months to October – although the same companies do expect output to rise slightly in the next few months.

There were also signs that inflationary pressure may be easing – although it remains elevated in historic terms. And they also expressed persistent concerns about a shortage of workers (although that particular problem may unfortunately disappear in a recession if more people lose their jobs and businesses produce less).

Alpesh Paleja, the CBI’s lead economist, said:

It’s a tough time for manufacturers. Price pressures remain acute, availability of materials is still a big issue – and it is 49 years since manufacturing firms were this worried about being able to find workers with the skills they need. It’s really no surprise that sentiment has deteriorated further.

Action to address the skills challenge is critical for the sector’s future prospects. Urgent reform to add flexibility to the apprenticeship levy would be an important first step for the new prime minister, which can rebuild confidence for manufacturers and restore momentum to their investment and growth ambitions.

HSBC boss expects to lead bank ‘for many years’ despite reshuffle

HSBC chief executive Noel Quinn has insisted the bank is not readying a succession plan after the surprise replacement of its chief financial officer.

There was “no change to my commitment” to the bank in light of the announcement, Quinn said. The bank promoted Georges Elhedery, the co-head of its global banking and markets division, to the finance position – and he has been tipped as a successor to Quinn.

Ewan Stevenson will be removed as HSBC’s chief financial officer in favour of Elhedery. Stevenson only joined HSBC in January 2019 after being poached from Royal Bank of Scotland.

Stevenson said on a call with journalists that he was not leaving because of a disagreement on strategy.

Elhedery, who joined in 2005, is co-chief executive of HSBC’s global banking and markets division.

It looks like some time away from banking benefited Elhedery. According to Reuters:

Elhedery’s sudden elevation comes after the 48-year-old took a six-month sabbatical from HSBC in January, citing a desire to travel with his family and explore personal interests.

HSBC also said it had considered Chinese shareholder Ping An’s proposal that it spin off its more profitable Asian business, and rejected the idea.

Liz Truss has just made her final address as prime minister in the latest stage of the strange handover of power to Rishi Sunak.

She said her time in office has left her “more convinced than ever that we need to be bold and confront the challenges that we face”.

You can follow the details – including Rishi Sunak’s forthcoming address to the nation this morning – on our politics live blog:

Adidas plans to end partnership with Kanye West – report

Adidas is planning to end its commercial partnership with Kanye West after the rapper made antisemitic comments, according to Bloomberg News.

Fashion brands Gap and Balenciaga have already dumped West – who now goes by the name Ye – after a string of controversies.

Here’s what Bloomberg said:

The German sports company may announce the move as early as Tuesday, according to people familiar with the matter, who asked not to be identified because discussions are private. A representative for Adidas didn’t immediately respond to requests for comment.

The Adidas decision follows weeks of deliberations inside the company, which over the past decade has built the Yeezy line — together with Ye — into a brand that’s accounted for as much as 8% of Adidas’s total sales, according to several estimates from Wall Street analysts.

Adidas has faced a deluge of criticisms for failing so far to end the partnership. You can read more details here:

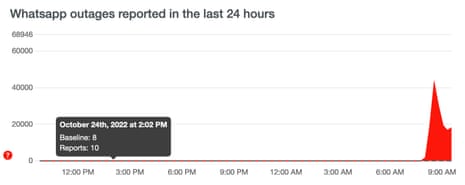

Bad news for Westminster plotters this morning: WhatsApp, the messaging platform, has gone down for users across the UK and around the world.

The platform, owned alongside Facebook by Meta, has suffered problems in the UK, Singapore and South Africa, according to data company Downdetector.

In a statement, a WhatsApp spokesperson said: “We’re aware that some people are currently having trouble sending messages and we’re working to restore WhatsApp for everyone as quickly as possible.”

Inflation for low-cost food ranges at 17%

The prices of low-cost ranges of vegetable oil and pasta have risen by more than 60% in the last year, according to data that attempts to track the impact of inflation on shoppers on a budget.

The Office for National Statistics (ONS) on Tuesday said the lowest-priced items have increased in cost by around 17% over the 12 months to September 2022: an increase from 7% over the 12 months to April 2022.

The index was instigated by Jack Monroe, a food writer and activist, who argued in January that the standard measure of inflation that “includes a leg of lamb, bedroom furniture, a television and champagne seems a blunt and darkly comical tool” for poorer households struggling to make ends meet.

The ONS notes that the data is “highly experimental” – they obtained it by scraping supermarket websites and the methodology is still being updated. Nevertheless, the findings show that prices of some popular carbohydrates have soared. Pasta and bread prices have likely been impacted by Russia’s invasion of Ukraine, which caused global wheat prices to surge.

The ONS noted that “Although not directly comparable, the rise in prices for the lowest-cost grocery items is similar to the 15% rise in the official measure of inflation for food and drink”. However, food costs are a much bigger chunk of poorer households’ income, so price rises on this scale will likely have more impact on the value ranges’ customers.

Groceries that have increased in price in the last year include:

🌶 vegetable oil by 65%

🍝 pasta by 60%

☕️ tea by 46%

🍟 chips by 39%

🍞 bread by 38%

🍪 biscuits by 34%In the last five months:

🌶 vegetable oil by 46%

🍟 chips by 24%

🍞 bread by 22% pic.twitter.com/ySo3Cahwl9— Office for National Statistics (ONS) (@ONS) October 25, 2022

Business confidence in Germany has dropped – but not by quite as much as expected by economists, according to a long-running index published by research institute Ifo.

The index fell from 84.4 to 84.3 points in October, above the 83.3 consensus according to a Reuters poll of economists. But it still highlights the worsening trend in the engine of the European economy: the same index was at 97.9 in October 2021, before Russia’s invasion of Ukraine sparked an energy crisis. Businesses are also markedly less optimistic for the coming months.

HSBC profits drop as it warns of inflation impacts ahead

There are hints of some of the challenges facing the soon-to-be prime minister in the third-quarter results from HSBC, the UK’s largest bank by share value: namely, the effects of rising interest rates and the likelihood of financial troubles for households.

However, for a bank the former is not necessarily a problem: as interest rates rise banks are able to fatten their margins by raising borrowing costs by more than the bump they give depositors.

But it is also having to put aside cash to cover potential defaults by borrowers. It warned that “Macroeconomic headwinds, including higher inflation and a weaker outlook, continue to weigh on the global economy”, although “credit indicators in our wholesale and retail portfolios remain relatively benign compared with historical levels”.

The Guardian’s banking correspondent, Kalyeena Makortoff, reports:

HSBC has reported better-than-expected profits for July to September after the bank reaped the benefits of surging interest rates that have raised borrowing costs for customers.

The London-headquartered lender said net interest income, which is the difference between what it charges for loans and pays in interest on deposits, jumped by a third to $8.6bn (£7.6bn) in the third quarter.

It benefited from climbing interest rates, including in the UK, where the Bank of England has increased rates to 2.25% from record lows of 0.1% last year, in an attempt to tackle inflation, which recently surged to 10.1%.

That helped HSBC report pre-tax profits of $3.2bn for the quarter, above average analyst estimates of $2.5bn.

While it marked a 42% drop in profits from the same period last year, the bank was facing tough comparisons. That was partly due to the fact that – like most lenders – HSBC was releasing cash that it had originally put aside for defaults during the Covid crisis last autumn.

HSBC said on Tuesday it had put aside $1.1bn to protect itself against potential defaults in the third quarter. That is more than the $884m that analysts had expected, and compares with the $659m it released last year.

The UK’s FTSE 100 has dropped on Tuesday morning after HSBC’s third-quarter results appeared to disappoint investors.

London’s benchmark stock market index has dropped by 0.4% in the opening 45 minutes of trading to below 7,000 points, with HSBC the biggest mover, down by 4.9%.

Sterling has edged up by 0.1% today against the US dollar to $1.1290 – just above the level on the day of the “mini-budget” that sunk Liz Truss’s ill-fated premiership and led to Sunak’s elevation. The pound has gained 0.2% against the euro.

The CBI’s Danker also pushed back against comments on Monday by Tory donor Guy Hands that the UK was “frankly doomed” without a renegotiation of the Brexit deal with the EU.

Hands, a private equity boss who backed remaining in the EU (but quit the UK for the low-tax Channel Islands), said mistakes since the referendum in 2016 had put the UK “on a path to be the sick man of Europe”.

Danker said:

If he is right then here we are in doom loop. I just don’t think he is right. We have got in this country the potential to lead the world in clean energy, in life sciences, in AI [artificial intelligence], in fintech. We have got growth potential.

What we can’t afford this time round is a government that doesn’t do whatever it takes to unlock that potential. That is, I’m afraid, the legacy of Brexit, it is the legacy of Covid, it is the legacy of the mini-budget. Yes, we need to stabilise things first and foremost, but if we don’t have a plan for growth then I’m afraid there aren’t good outcomes in the next decade.

Lobby group boss calls for growth policies from Rishi Sunak

Good morning, and welcome to our live, rolling coverage of business, economics and financial markets.

The boss of Britain’s largest business lobby group has warned incoming prime minister Rishi Sunak against pursuing an austerity “doom loop” which he said could lead to a repeat of the weak economic growth since the financial crisis.

Tony Danker, head of the Confederation of British Industry (CBI), said that Sunak would have to look at policies such as planning reform or liberalising immigration that might be unpopular with the Conservative party’s members.

Sunak will meet King Charles on Tuesday to be invited to form a government after Liz Truss ends her briefest of reigns at the top of the UK government. Truss had pursued a dash for growth with a radical tax-cutting “mini-budget” that resulted in financial market chaos and her resignation in less than two months.

Danker had initially backed Truss’s ambition to grow the UK economy, but he has since acknowledged that fiscal stability should be the priority. However, on Tuesday he told the BBC’s Today programme that a growth strategy remains important. He said:

The 2010s began with some austerity and were then ensued with very low growth, zero productivity and low investment. It wasn’t a successful strategy for growth.

We’re going to find out on Monday that if all there is is tax rises and spending cuts and there’s nothing in there about growth the country could end up in a similar doom loop where all you have to do is keep coming back every year to find more tax rises and more spending cuts because you’ve got no growth.

Danker argued that Sunak and the Conservatives do have tools at their disposal to boost growth even if they do not ease the fiscal taps.

If you’re going to [not cut taxes or spend on big projects] – and you must – then I’m afraid I don’t think you can hold on to those policies that would have been Conservative favourites but now result in our economy getting worse and worse if you’re not prepared to deploy them.

He said “planning permission, immigration, regulation: they become incredibly important”.

Meanwhile, the big corporate news of the morning is HSBC has reported falling profits as the UK’s largest bank put aside $1.1bn to cover possible loan losses. But those results were better than expected as higher interest rates allow it to reap higher margins on its loans.

Noel Quinn, HSBC’s chief executive, described it as “strong momentum in the third quarter” and “a good set of results”.

There was also the surprise news of the ousting of chief financial officer Ewan Stevenson in favour of Georges Elhedery, the former head of HSBC’s investment bank. More on that in a bit.

The agenda

-

9am BST: Germany Ifo business climate (October; previous: 84.3 points; consensus: 83.3)

-

11am BST: UK Confederation of British Industry (October; prev.: -2; cons.: -12)

-

3pm BST: US consumer confidence (October; prev.: 108; cons.: 106.5)

https://www.theguardian.com/business/live/2022/oct/25/hsbc-profits-european-gas-prices-weather-ftse-100-cbi-rishi-sunak-business-live Investors buy UK bonds amid hope for calm under Rishi Sunak – business live | FTSE